Many homeowners think that once they take out an initial mortgage for a set period of time, they don’t have to worry about taking out a mortgage again. However, you may find that it’s beneficial to refinance your home several years down the road. As mortgage brokers Las Vegas will tell you, refinancing can provide several benefits, including taking advantage of better interest rates and saving money. If you’re wondering what refinancing means and if you’re qualified, expert mortgage brokers Las Vegas share their tips and guidance.

What is Refinancing?

What is Refinancing?

Refinancing a home essentially means that you replace an existing loan with a new one. There are many reasons why it might make sense to make the change. One reason is to get a lower interest rate than what you are currently paying. When you add up the amount you save on lower interest rates over time, the cost savings on a multi-year loan can be tremendous!

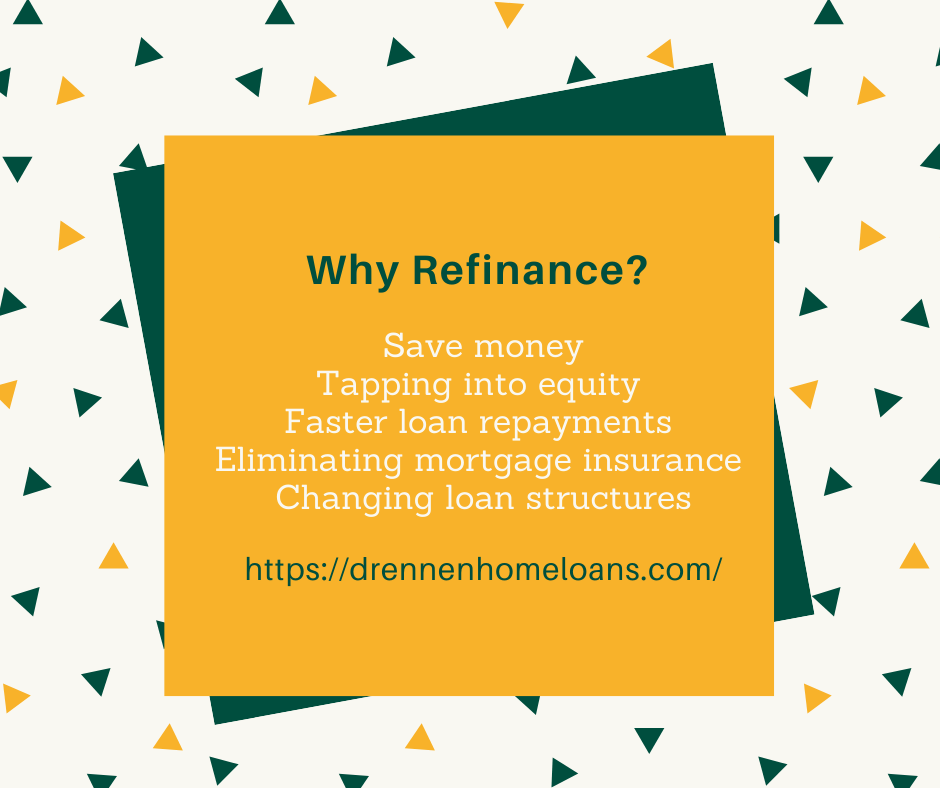

Why Should You Refinance?

Along with simply saving money and lowering your monthly payments, refinancing gives you the opportunity to make improvements to your home.

Other key benefits of refinancing include:

- Tapping into equity

- Faster loan repayments

- Eliminating mortgage insurance

- Changing loan structures

Refinancing makes it possible to withdraw larger amounts of cash to help with home improvement needs, such as renovations or additions. Another major advantage to refinancing is that it might make it easier to pay off a loan faster. Initially, homeowners often start with a longer-term loan, such as a standard 30-year loan. Refinancing, however, can let you change to a 15-year loan instead. While your monthly payments may increase with a shorter loan period, you end up paying less money in interest throughout the loan. This is especially true with fixed-rate home loans Las Vegas, which tells you upfront exactly how much money you can expect to pay in interest throughout a loan, as the loan rate is locked in when the loan begins. If you have Federal Housing Administration (FHA) mortgage insurance on your primary loan, refinancing can help you eliminate mortgage insurance payments. Keep in mind that refinancing may not allow you to eliminate any private mortgage insurance that you have on a conventional loan. However, you can still eliminate private insurance if you build up at least 20% in home equity. In the event that you need to file for bankruptcy, refinancing can help reduce the financial burden as well. Finally, a refinance gives you a chance to change your loan structure, generally from a variable-rate to a fixed-rate loan.

Is There a Good Time to Refinance?

Is There a Good Time to Refinance?

While you can consider refinancing at any time, experts recommend making the change when interest rates drop below what you’re currently paying. Ideally, if you can lower your interest rate by at least .5%, you may find it advantageous to refinance. A mortgage company Las Vegas can help you determine your interest rate compared to current market rates, which in turn gives you a better understanding of when to refinance and how much money you’ll save.

Credit score is another major factor in determining loan payments. While you can still qualify for certain loans with a lower credit score, such as government-backed loans, you may end up paying more in interest as a result. Furthermore, most loans available to individuals with a sub-par credit score or lower income require you to pay mortgage insurance as well. This protects the lender in case you default on your mortgage. You may also want to consider refinancing when your credit score improves.

Converting a Loan

As with an initial loan, you can choose between a fixed-rate and a variable-rate loan when you refinance a home. Often, homeowners choose to transition from adjustable rate mortgages Las Vegas to fixed rate home loans Las Vegas when they refinance. Interest rates on a fixed-rate loan are not guaranteed from the start, which means that you might end up paying more or less on interest in any given month. Generally, interest rates in variable-rate loans go up over time. A fixed-rate loan, in contrast, has an interest rate that does not change. This ensures predictable monthly payments and more financial stability.

How to Refinance a Mortgage

Now that you know the benefits of refinancing, you may be ready to start the refinancing process.

There are several key steps to follow when refinancing a mortgage, including:

- Setting a goal

- Shopping for rates

- Submitting an application

- Choosing a lender

- Setting an interest rate

- Closing the loan

First, it’s important to set a goal, which is the main reason why you’re considering refinancing. This can be to eliminate mortgage insurance, tap into equity, shorten a loan term, or all of the above! Shopping around and doing research helps you find the best refinance rate available. Look out for added fees too, which can add on a surprising amount of money to your refinance. Experts recommend applying for a loan with at least three lenders, and ideally up to five. Another tip: submit your applications within two weeks of each other to lower the impact on your credit score. Comparing a Loan Estimate document helps you determine the best offer and most suitable lender. After choosing a lender, try to close the loan within a time period that gives you an optimal interest rate. Once that happens, you’ll close the loan, which also means paying the costs listed in the Closing Disclosure and Loan Estimate. Ultimately, refinancing a home is much like taking out an initial loan, with the exception that you already have the keys to your home.

Refinancing a home has many benefits, from shortening a loan duration to helping you get more favorable interest rates and make necessary improvements to your home. If you’re considering refinancing, don’t hesitate to contact us for assistance. We will gladly walk you through the refinancing process and help you determine if refinancing is a good option for your situation.