What Are Home Mortgage Interest Rates Right Now?

As a loan officer in Las Vegas will tell you, home mortgages come in many forms. Some of the most common kinds are adjustable-rate, fixed-rate, FHA, jumbo, and VA. Each type of mortgage has its unique advantages and is ideal for a particular type of borrower. Whether you already know that you want a fixed-rate mortgage, you prefer the flexibility of a mortgage with a variable interest rate, or you need help finding the right mortgage for you. A loan officer in Las Vegas can provide helpful information on home mortgages to best suit your needs.

30-Year Fixed-Rate Mortgage

30-Year Fixed-Rate Mortgage

A 30-year fixed-rate mortgage is the most popular type of home mortgage. Because it has a long term of 30 years, you can expect to have low monthly payments compared to shorter-term loans. Additionally, because the interest rate is locked in, you’ll know exactly how much money you will spend each month on mortgage payments. A long-term fixed-rate mortgage is ideal for homeowners who plan to stay in their homes for an average of seven to 10 years. Although this type of mortgage has a set term of 30 years, many mortgage brokers Las Vegas give you the option to make higher monthly payments to pay off the mortgage sooner, which lowers your interest payments and overall mortgage expenses.

15-Year Fixed-Rate Mortgage

The second most common (and popular) of all mortgages in Las Vegas is a 15-year fixed-rate mortgage. This type of mortgage is similar to a 30-year mortgage, except that you’ll make slightly higher monthly payments to pay off the loan faster. Ultimately, you can save money on interest by choosing a mortgage with a 15-year term instead of a 30-year term. A 15-year fixed-rate mortgage also has a locked-in interest rate, which gives you greater predictability for your loan payments. This type of mortgage is often used for refinancing.

Adjustable-Rate Mortgage

An adjustable-rate mortgage is a home loan with an initial fixed-rate followed by a rate that fluctuates periodically. For instance, some loans have a fixed interest rate for five years, followed by an interest rate that changes each year. Many people enjoy the loan’s initial low monthly payments, which can be locked in for one, five, seven, and up to 10 years. An adjustable-rate mortgage is ideal for homeowners who don’t intend to have the mortgage for a long time.

FHA Mortgage

A Federal Housing Administration (FHA) mortgage is a government-backed mortgage. This type of mortgage is geared toward individuals who have lower incomes. FHA loans provide many benefits for lower-income home buyers, including a small down payment of just 3.5%. Additionally, FHA mortgages are accessible to people who have lower credit scores than are usually required for a mortgage, which may be as low as 500.

Conventional Mortgage

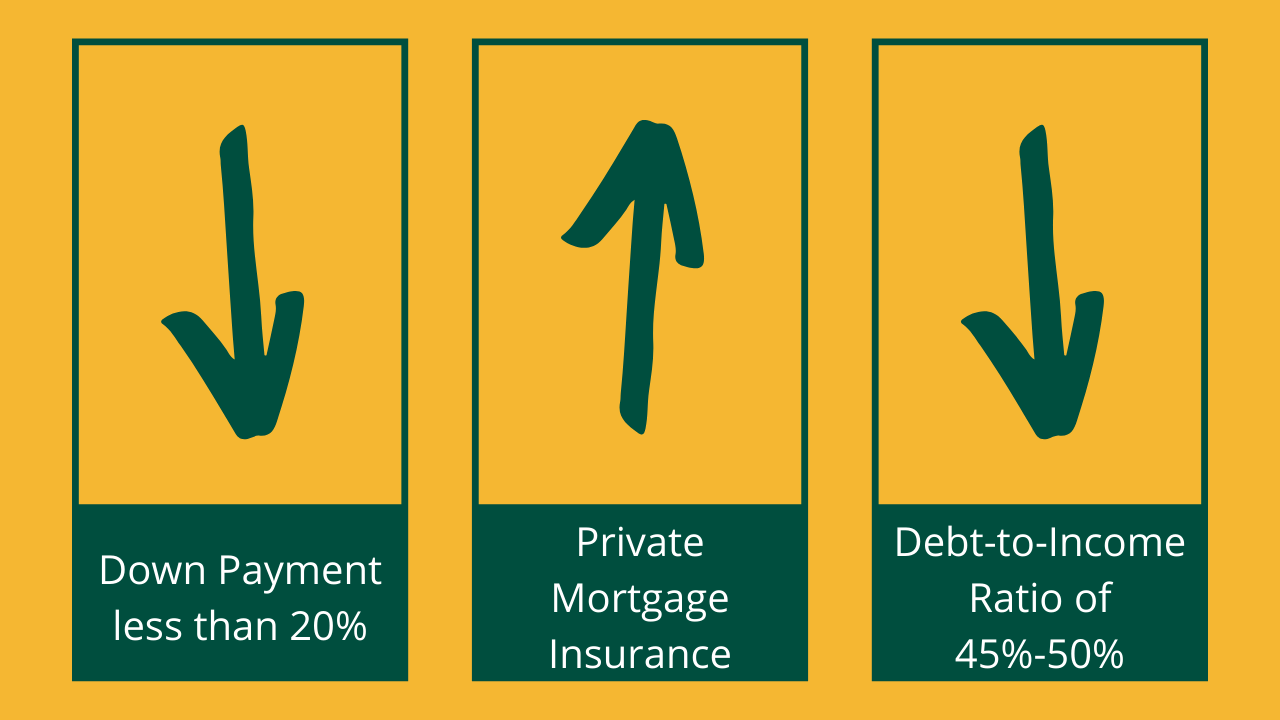

Conventional mortgages are defined as loans that are either conforming or non-conforming. Conventional mortgages are backed by private lenders rather than the federal government. Conforming loans fall within the maximum limits established by Fannie Mae or Freddie Mac, the two government agencies that back most mortgages in the United States. Non-conforming loans are another option. The most common type of non-conforming loans are called jumbo loans. Conventional mortgages may also be available for homeowners who have lower income levels, as they require a down payment of less than 20%. However, keep in mind that loans with lower down payment rates often require you to purchase private mortgage insurance. Additionally, most require a debt-to-income ratio of 45% – 50% to qualify. (Read the complete home buyers guide here.)

Conventional mortgages are defined as loans that are either conforming or non-conforming. Conventional mortgages are backed by private lenders rather than the federal government. Conforming loans fall within the maximum limits established by Fannie Mae or Freddie Mac, the two government agencies that back most mortgages in the United States. Non-conforming loans are another option. The most common type of non-conforming loans are called jumbo loans. Conventional mortgages may also be available for homeowners who have lower income levels, as they require a down payment of less than 20%. However, keep in mind that loans with lower down payment rates often require you to purchase private mortgage insurance. Additionally, most require a debt-to-income ratio of 45% – 50% to qualify. (Read the complete home buyers guide here.)

Government-Insured Mortgages

Several government agencies back loans. In addition to the Federal Housing Administration, the U.S. Department of Agriculture (USDA) and the U.S. Department of Veterans Affairs (VA) also back loans. VA loans are available to veterans or active members of the U.S. Military. VA loans do not require a down payment. They also have a capped closing cost, which may even be paid by the seller. VA loans are often accompanied by a funding fee, which is a percentage of the initial mortgage amount that offsets the program’s cost. The fee can typically be paid upfront or at closing. USDA loans allow borrowers with low to moderate incomes the opportunity to purchase homes in rural areas. To qualify, borrowers must buy property in an area eligible for USDA loans. Borrowers must also have a certain income level to qualify. Like VA loans, some USDA loans do not require a minimum down payment. Government-backed loans help borrowers finance a home if they don’t otherwise qualify for a conventional mortgage. They’re also available to first-time home buyers as well as repeat buyers. Government-backed loans can often be secured by individuals with a credit score that is below the average requirement, too.

Finding The Most Suitable Mortgage Program

From long-term loans to loans backed by the government, there are many types of mortgages available to homeowners. Contact us today to learn more about the mortgages available for your home purchase and find out which one is best for you.